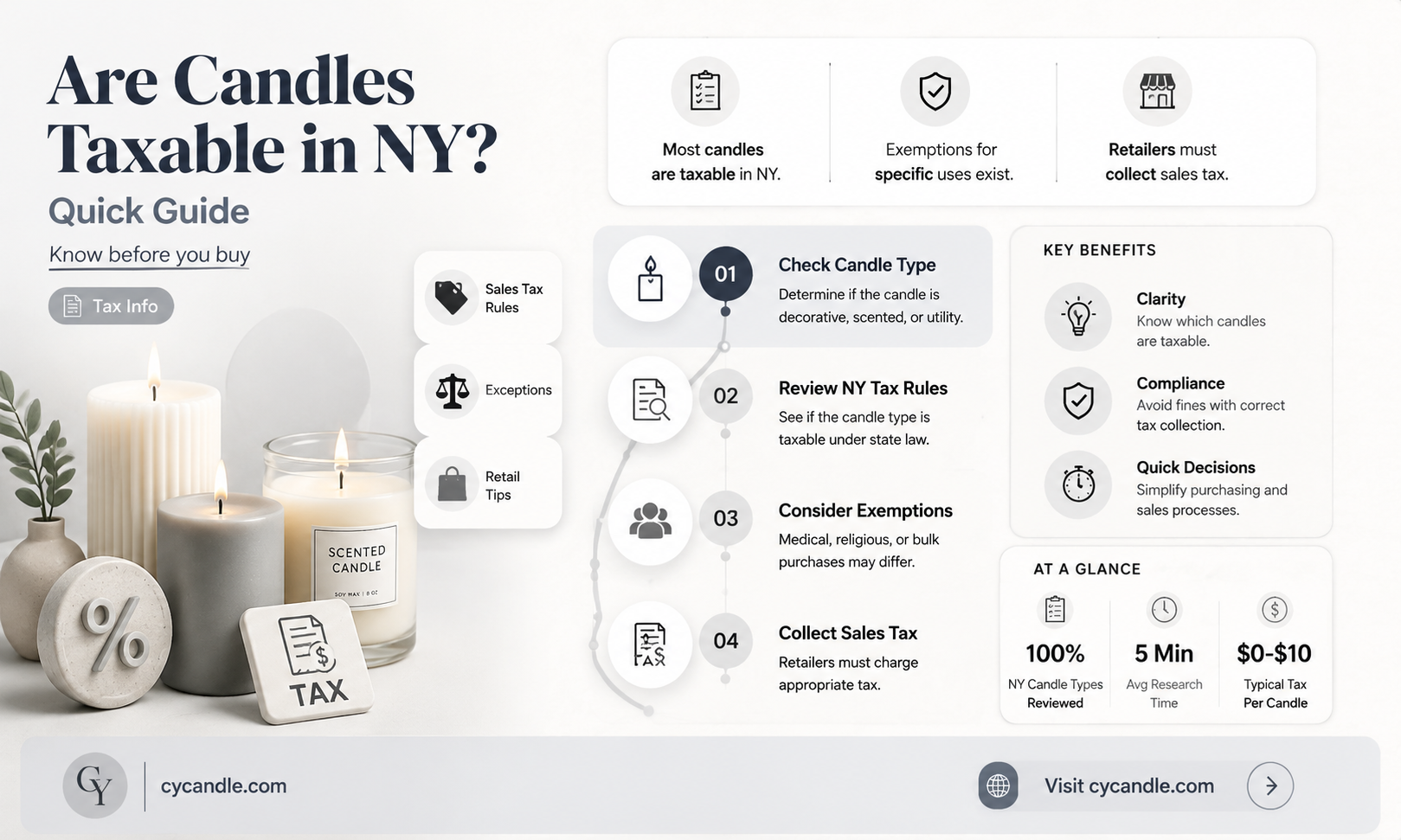

New York State imposes sales tax on the sale of tangible personal property and services. However, there are several exemptions to this rule. For example, clothing and footwear priced under $110 are exempt from sales tax. Businesses that sell taxable items and services and ship them to New York are required to collect and remit sales tax. This includes businesses that sell candles.

| Characteristics | Values |

|---|---|

| Are candles taxable in New York State? | Yes |

| New York State sales tax rate | 4% base rate |

| Local sales tax rate in New York City | 4.5% |

| Transportation tax in New York City | 0.375% |

| Combined sales tax rate in New York City | 8.875% |

| Clothing and footwear exemption | Priced under $110 per item |

Explore related products

What You'll Learn

- Are candles taxable in New York State if they are purchased wholesale?

- Are candles taxable in New York State if they are for personal use?

- Are candles taxable in New York State if they are sold online?

- Are candles taxable in New York State if they are sold in a restaurant?

- Are candles taxable in New York State if they are sold in a brick-and-mortar store?

![]()

Are candles taxable in New York State if they are purchased wholesale?

In New York State, sales of tangible personal property are subject to sales tax unless specifically exempt. Sales of services are generally exempt from New York sales tax unless they are specifically taxable. Tangible personal property refers to any kind of physical personal property that has a material existence and is perceptible to the human senses.

New York charges sales tax on any transaction where tangible personal property or services are transferred. However, the state has a number of sales tax exemptions. For example, services are generally exempt, unless specifically taxable. Certain clothing and footwear sold for less than $110 per item are exempt from sales tax in New York State.

Sales tax is a tax assessed on the sale of a product to the end-user. Raw materials used to manufacture a product and goods purchased at wholesale can be purchased without paying sales tax if you are registered as a reseller. If, however, you purchase materials free of sales tax but do not use them in your manufacturing process or for resale, you are probably required by your state or local taxing authority to pay a "Use Tax" on those materials because you became the end-user.

CandleScience, a company that sells candle-making supplies, collects sales tax on orders shipping to New York State. This indicates that candles are taxable in New York State. If a company like CandleScience sells candles at wholesale, and the purchaser is registered as a reseller, then no sales tax would be collected. However, if the purchaser does not use the candles for resale, they may be required to pay a "Use Tax" on those candles.

Candles and Carbon Monoxide: What's the Link?

You may want to see also

Explore related products

![]()

Are candles taxable in New York State if they are for personal use?

Candles are taxable in New York State if they are considered tangible personal property. This means that any physical personal property that can be perceived by the human senses is subject to sales tax in New York. However, there are certain exemptions to this rule, and it is important to consult the state's tax publications and bulletins for specific information.

The New York State sales tax rate is currently 4%, but local jurisdictions can add to this rate, resulting in varying total rates across the state. For example, New York City has a local sales tax rate of 4.5%, plus a transportation tax of 0.375%combined rate of 8.875% within the city.

In addition to the sales tax on tangible personal property, New York also charges sales tax on certain services, such as interior decorating and transportation services. However, services are generally exempt from sales tax unless they are specifically taxable.

When it comes to candles, it is important to note that sales tax may apply if the purchase is made within New York State or if the candles are brought into the state by a New York resident. This is known as the New York State use tax, which applies to taxable items or services purchased outside of New York and then brought into the state.

Overall, it appears that candles for personal use may be subject to sales tax in New York State, depending on the specific circumstances of the purchase and the location of the buyer. It is always advisable to consult the official tax publications and bulletins provided by the state to determine the exact tax liability for any given transaction.

Candle Shops: A Successful Business Venture?

You may want to see also

Explore related products

![]()

Are candles taxable in New York State if they are sold online?

In New York State, sales tax is charged on any transaction where tangible personal property or services are transferred. Tangible personal property is defined as any kind of physical personal property that has a material existence and is perceptible to the human senses.

Candles are considered tangible personal property, and therefore, sales of candles are subject to New York sales tax unless they are specifically exempt. This means that if you are selling candles online and shipping them to customers in New York, you are required to collect and remit sales tax on those transactions.

However, there are certain sales tax exemptions in New York State. For example, certain clothing and footwear sold for less than $110 per item are exempt from sales tax. Additionally, food that is sold unheated and in a similar way to how it would be found in a grocery store or supermarket is not taxable.

It is important to note that sales tax laws can be complex and may change over time. Therefore, it is always recommended to consult the official New York State tax website or seek professional tax advice to ensure compliance with the latest regulations.

The Ultimate Guide to Understanding "Couldn't Hold a Candle" Synonyms

You may want to see also

Explore related products

![]()

Are candles taxable in New York State if they are sold in a restaurant?

In New York State, sales of tangible personal property are generally subject to sales tax unless specifically exempt. Sales of services are generally exempt from sales tax unless specifically taxable. Tangible personal property refers to any kind of physical personal property that has a material existence and is perceptible to the human senses.

Candles are considered tangible personal property, and as such, sales of candles in New York State are generally subject to sales tax. This includes candles sold in restaurants. However, there may be certain exemptions or special considerations for sales made in restaurants or other specific contexts.

In New York, the restaurant tax is the state's general local and state tax rate, but certain items sold in restaurants may be exempt from taxes. For example, food that is sold unheated and in a similar state to how it would be found in a grocery store or supermarket is not taxable. On the other hand, food consumed on the premises, including in a food court or at picnic tables outside a drive-in restaurant, is always taxable.

It is important to note that sales tax laws and exemptions can vary across different jurisdictions within New York State, and local jurisdictions can levy additional sales taxes on top of the base state sales tax rate. For example, New York City has a local sales tax rate of 4.5%, resulting in a combined rate of 8.875% within the city when including the transportation tax.

Businesses selling candles in New York State, including those sold in restaurants, should consult the relevant tax authorities and publications to ensure they are complying with the applicable sales tax regulations and exemptions.

Dollar General Birthday Candles: A Quick Guide

You may want to see also

Explore related products

![]()

Are candles taxable in New York State if they are sold in a brick-and-mortar store?

In New York State, sales tax is charged on any transaction where tangible personal property or services are transferred. Tangible personal property refers to any kind of physical personal property that has a material existence and is perceptible to the human senses.

Candles are considered tangible personal property, and therefore, sales of candles are subject to New York sales tax unless specifically exempt. This means that if you are selling candles in a brick-and-mortar store in New York State, you are generally required to collect sales tax from your customers.

However, there are certain exemptions to sales tax in New York State. For example, clothing and footwear priced under $110 per item are generally exempt from sales tax. Additionally, if you are a reseller, you may be able to purchase raw materials used to make candles without paying sales tax by providing a resale certificate.

It is important to note that sales tax laws can be complex and may change over time. Therefore, it is always recommended to consult the New York State Department of Taxation and Finance or a tax professional for the most up-to-date and accurate information regarding sales tax on candles or any other specific item.

To comply with sales tax requirements in New York State, businesses typically need to obtain a Certificate of Authority, which grants them the right to collect tax and accept sales tax exemption certificates. This certificate can be obtained through the New York Business Express website, and it is recommended to apply at least 20 days in advance.

Unwind with Haven St. Candle Co's Relaxing Scents

You may want to see also

Frequently asked questions

Yes, candles are taxable in New York State.

Sales tax is a tax assessed on the sale of a product to the end-user.

New York State has a base sales tax rate of 4%. Local jurisdictions can levy additional sales taxes, leading to varying total rates across the state. For example, New York City applies a local sales tax of 4.5%.

Yes, certain items are exempt from sales tax in New York State. For example, clothing and footwear priced under $110 are exempt from sales tax.

If your business has a physical presence in New York State, you are generally required to collect and remit sales tax on all taxable sales. If your business is based outside of New York State but sells products that are shipped into the state, you may also be required to collect sales tax if you meet certain economic thresholds.